Introduction

Soy protein isolate (SPI) continues to strengthen its position as a high-value plant-based ingredient and a critical platform chemical in the global protein economy. As of 2026, the SPI supply chain reflects a tightly integrated system linking soybean cultivation, crushing facilities, and high-purity protein extraction units. With global market growth tracking a CAGR of ~7.2%, SPI pricing has stabilized in the range of USD 2,800–4,200/MT, driven by sustained demand from food, feed, and nutraceutical sectors. Annual global production is estimated at nearly 1.4–1.8 million MT, concentrated in North and South America and expanding rapidly in Asia.

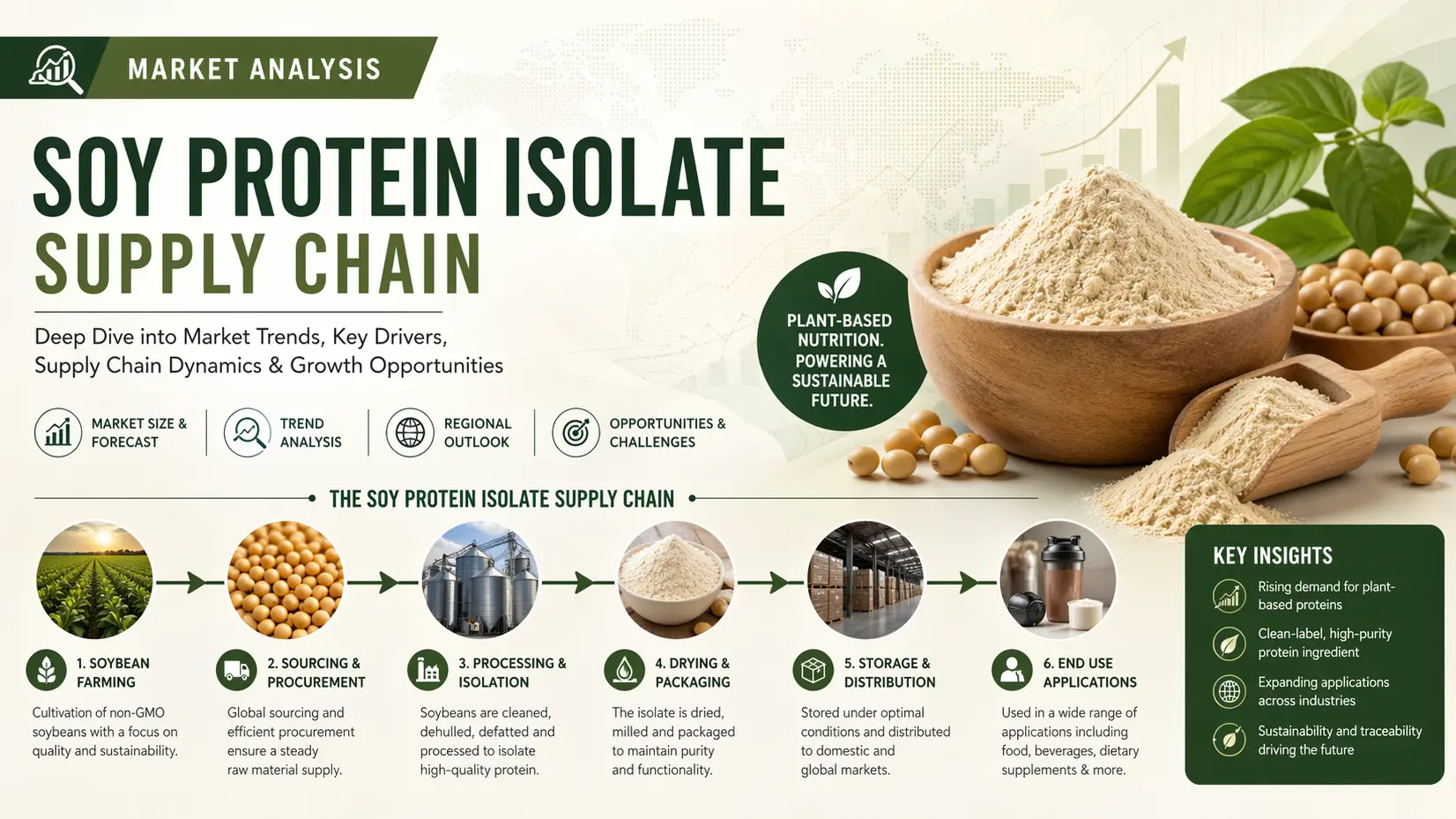

Soybean Origin and Raw Material Concentration

The SPI supply chain begins with soybean cultivation, where Brazil, the United States, and Argentina dominate over 75% of global output. This concentration introduces structural dependency on climate and export policy shifts. In 2026, soybean meal crushing capacity exceeds 370 million MT globally, yet only a small fraction is upgraded into isolate-grade processing. This imbalance creates raw material volatility, directly influencing SPI margins and procurement strategies for downstream processors.

Processing Infrastructure and Yield Economics

SPI production relies on advanced aqueous extraction and membrane filtration systems, where yield efficiency typically ranges between 65–70% protein recovery. Capital-intensive facilities in China and the U.S. are driving scale efficiencies, yet operational costs remain elevated due to energy and enzymatic processing inputs. Production costs fluctuate around USD 1,900–3,000/MT, with margin sensitivity increasing as feedstock prices move. Technological upgrades are gradually improving output consistency and reducing protein denaturation losses.

Global Logistics and Trade Route Dependencies

SPI distribution is highly export-driven, with bulk shipments moving from the Americas to Asia-Pacific and Europe. Containerized trade has become essential due to moisture sensitivity and shelf-life constraints. Freight volatility in 2026 continues to influence landed costs, particularly in Southeast Asia, where import dependency exceeds 60%. Trade bottlenecks at key ports in China and the Netherlands also contribute to periodic supply tightening and inventory buffering strategies among buyers.

End-Use Industries and Demand Synchronization

Demand is primarily driven by plant-based food manufacturers, sports nutrition brands, and aquafeed producers. Food-grade SPI accounts for nearly 55% of total consumption, supported by rising protein fortification trends. Feed applications are expanding steadily, especially in aquaculture, where SPI is replacing fishmeal alternatives. Synchronization between production cycles and retail demand remains a challenge, pushing buyers toward long-term contracting and integrated sourcing models.

Conclusion

As SPI evolves as a platform chemical for high-value protein systems, supply chain resilience becomes a decisive competitive factor. Companies are increasingly prioritizing vertically integrated sourcing, regional warehousing, and contract manufacturing to mitigate volatility across raw materials, processing, and logistics. In this context, Tradeasia International emerges as a reliable global solution provider, enabling seamless chemical and ingredient sourcing across fragmented markets while supporting consistent SPI supply continuity for industrial buyers.

Sources

-

https://www.fao.org/soybean-economy

-

https://www.ers.usda.gov/topics/crops/soybeans-oil-crops/

-

https://www.grandviewresearch.com/industry-analysis/soy-protein-isolate-market

Leave a Comment