Global Soy Lecithin Supply Chain Dynamics and Market Shifts in 2026

Introduction: Repositioning Soy Lecithin in Global Supply Networks

Soy lecithin continues to strengthen its position as a critical phospholipid-based emulsifier across food processing, animal nutrition, and pharmaceutical formulation supply chains in 2026. As a by-product of soybean oil refining, its availability remains tightly linked to global crushing activity in Brazil, the United States, and Argentina, which together account for more than 75% of feedstock supply. The market is expanding at an estimated 4.8% CAGR, supported by clean-label demand and industrial formulation growth. Average export prices range between USD 1,250–1,650/MT, reflecting tightening logistics and quality premiums.

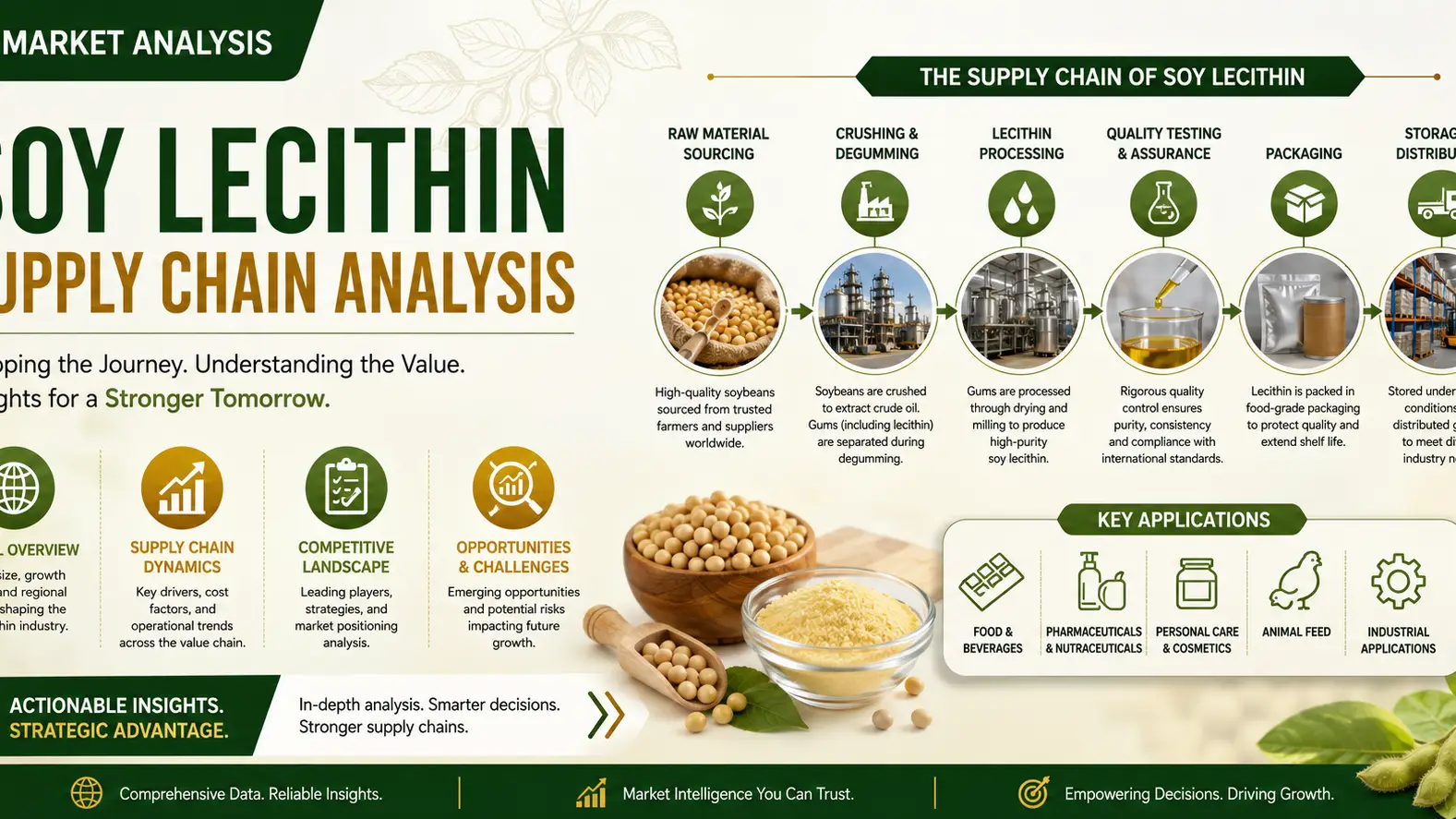

Raw Material Sourcing and Crushing Hub Concentration

Soy lecithin supply chain resilience begins with soybean crushing dominance concentrated in South America and North America. Brazil alone contributes nearly 35% of global soybean output, followed closely by the United States at 28% and Argentina at 12%. This geographic clustering creates dependency risks, especially during climate disruptions and export restrictions. In 2026, crushing volumes are projected to exceed 410 million MT of soybeans globally, directly influencing lecithin availability and downstream pricing stability in international markets.

Processing, Degumming and Refining Efficiency Trends

Refining efficiency in soy lecithin extraction is increasingly driven by enzymatic degumming and membrane separation technologies, improving phospholipid recovery rates across major processors. In 2026, average yield efficiency has improved by 6–8%, reducing waste streams and enhancing crude lecithin output consistency. Production hubs in China and the EU continue to modernize facilities, collectively accounting for nearly 1.1 million MT annual lecithin processing capacity, while cost of processing remains stable at around USD 180–220/MT soybean input equivalent.

Trade Flows, Logistics and Price Volatility

Global soy lecithin trade flows are increasingly shaped by container logistics constraints and tariff-sensitive routes between South America, Asia, and Europe. Freight normalization in 2026 has eased volatility, yet spot pricing remains reactive to soybean oil margins. Export benchmarks fluctuate between USD 1,250–1,650/MT, while bulk contracts from Brazil and the U.S. dominate 62% of global trade. Shipping lead times average 28–35 days, impacting procurement strategies for mid-sized formulators and distributors.

End-Use Demand and Buyer Landscape Evolution

Demand for soy lecithin continues to expand across food manufacturing, bakery applications, and animal feed premixes, where it serves as a natural emulsifier and wetting agent. In 2026, food-grade consumption represents over 58% of total demand, driven by clean-label reformulation trends in Europe and Asia. Global consumption is estimated at 3.2 million MT annually, with multinational food processors and feed integrators accounting for the majority of procurement contracts across structured supply chains.

Conclusion

As soy lecithin consolidates its role in global formulation industries, supply chain agility, feedstock security, and processing innovation will define competitive advantage through 2026. With tightening margins and rising specification demands, buyers are increasingly seeking integrated sourcing partners. In this evolving landscape, Tradeasia International offers end-to-end chemical distribution support, ensuring reliable access, optimized logistics, and consistent product quality across global markets.

Sources

Leave a Comment