Global Deoiled Rice Bran Supply Chain 2026: From Milling Residue to Strategic Feed Commodity

Introduction: Deoiled Rice Bran as a Platform Ingredient

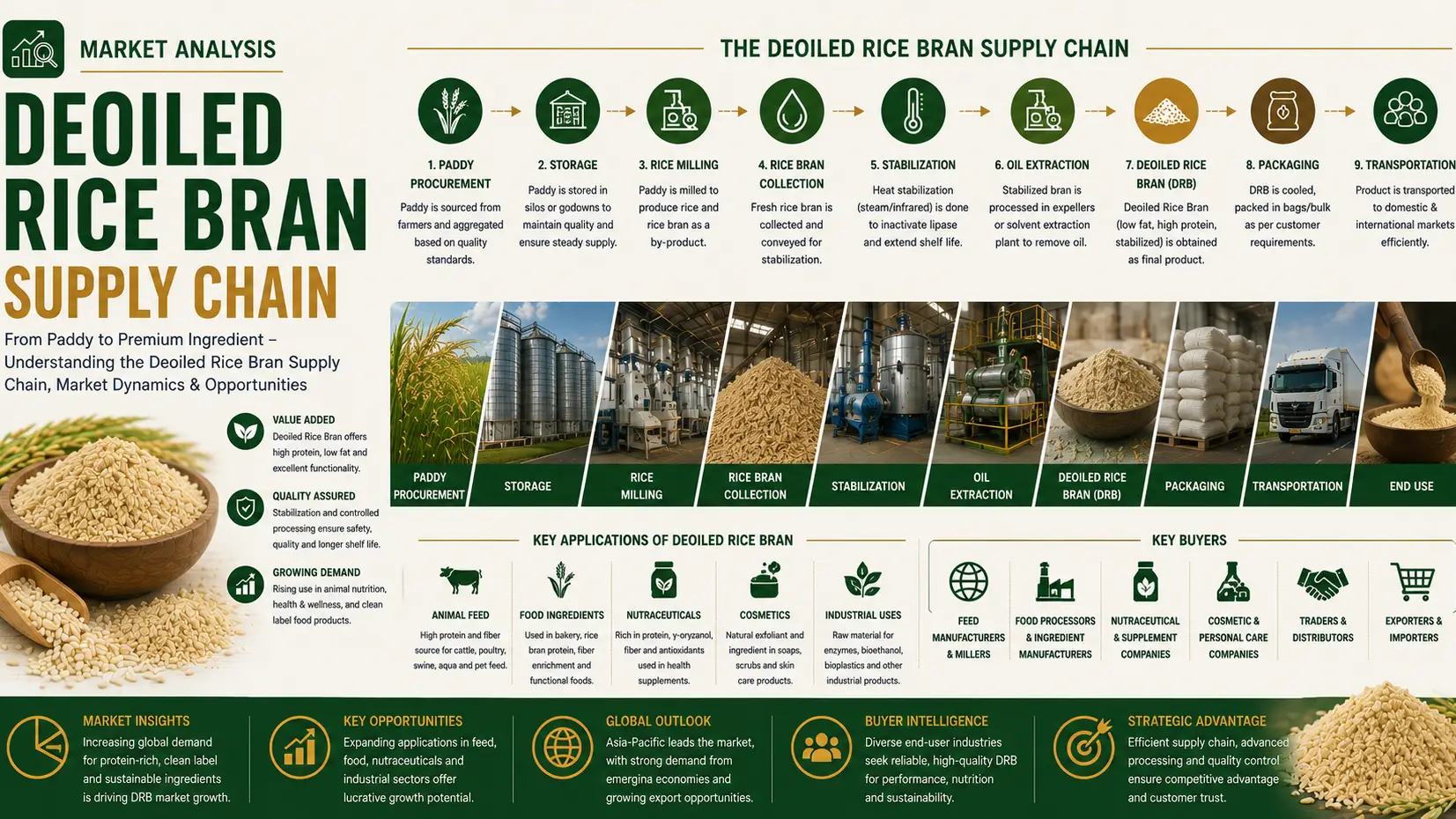

Deoiled rice bran (DORB) has evolved beyond a milling residue into a globally traded feed and bio-based platform ingredient. In 2026, the market reflects tightening grain balances and stronger demand from livestock and aquaculture industries. Global output is estimated at 48–52 million metric tons, derived from expanding rice milling activity across Asia. The market is growing at a steady 4.3% CAGR, supported by its high protein value (15–18%) and cost competitiveness against traditional feed meals. Average global pricing ranges between 180–240 USD/MT, depending on protein enrichment and regional availability.

Supply Concentration and Milling-Origin Dependency

The supply chain remains highly concentrated in Asia, with India, China, Vietnam, and Thailand collectively accounting for more than 70% of global production. Deoiled rice bran availability is directly linked to rice milling cycles, making it a structurally seasonal commodity. Milling efficiency improvements have increased extraction yields by nearly 8–10% over the past five years, stabilizing supply but not eliminating volatility during poor harvest seasons.

Logistics, Storage, and Export Trade Corridors

Storage remains a critical bottleneck due to the product’s high free fatty acid content, which limits shelf life. Export-oriented supply chains rely heavily on coastal aggregation hubs in India and Southeast Asia. Containerized exports to the Middle East and Europe have increased, with logistics costs contributing up to 12–18% of landed price. Cold-chain-adjacent storage innovations are gradually improving export stability.

Demand Structure Across Feed and Bio-Based Industries

The primary demand driver remains the animal feed sector, especially poultry and cattle nutrition, absorbing nearly 65% of global volumes. In parallel, emerging biofuel and fermentation applications are expanding industrial demand. Ethanol blending programs in Asia have begun integrating deoiled rice bran derivatives as supplementary feedstock inputs, diversifying its end-use profile.

Pricing Volatility and Market Margin Pressures

Price movements are closely tied to rice paddy procurement cycles and crude rice bran oil demand. In 2026, volatility remains moderate, with spreads influenced by freight rates and oil extraction margins. Market participants continue to face compression as feed integrators push for bulk procurement contracts, limiting spot-market premiums.

Conclusion: Strategic Positioning and Tradeasia Role

As deoiled rice bran continues to mature as a platform feed ingredient, supply chain integration and cross-border trade efficiency will define competitive advantage. With increasing demand diversification and tightening agricultural cycles, stakeholders are shifting toward reliable sourcing partnerships. In this evolving landscape, Tradeasia International positions itself as a global solutions provider, enabling consistent procurement, optimized logistics, and integrated commodity distribution across feed and agro-industrial markets.

Sources

Leave a Comment